Sunday, November 10, 2024

Tuesday, October 29, 2024

A Strategy of Highest-Value Deployment of Nuclear Energy in the Philippines

(Through Nuclear Powered Hyperscale Data Centers)

The Advent of Nuclear Powered Hyperscale Data Centers (HDC)

Nuclear Powered HDCs are currently (2024) being developed in the United States. The major players in the global HDC sector are already contracting with nuclear power providers to fulfill the high-demand and high-reliability electricity required by HDCs. These include:

What is driving the growth of HDCs?

In short, the internet. Today, the internet is an integral part of any commercial enterprise and, indeed, the everyday life of most individuals on earth. We rarely contemplate the underlying infrastructure requirements to enable the internet to function globally, which are massive and complex.

Think surfing the internet, social media, shopping online, paying bills online, customer services online, business process outsourcing, remote working, government services online, education online, Cloud apps and storage, securing a ride through Grab, conducting a video conference call on Viber or any number of similar apps, Netflix, YouTube, Spotify, Alexa among other virtual assistants, gaming online, gambling online, internet porn, ChatGPT among other AI apps and so on. All these and more are seamlessly delivered by a global network of submarine and terrestrial fiber optic cables (known as fiber optic backbones or networks), wireless broadband networks (like 5G and beyond), satellite broadband networks (like Starlink) and an astronomical number of servers housed in climate-controlled data centers all over the world.

Over the years, the massive and ever-increasing volumes of data that need to be processed to fulfill said internet-based online services have spurred the growth of HDCs–each requiring large tracts of land, housing thousands of servers and having power demands in the range of 100 MW. More recently, due to the increasing adoption of AI-related technologies and applications all over the world, this demand for even more computing capacity is catalyzing major players in the HDC sector to develop more and larger HDCs.

HDCs, Renewable Energy and “Green” Nuclear Power

Due to its high electricity demands, the HDC sector has taken the lead in securing most (in some cases, all) of its electricity supply from renewable energy facilities such as solar farms, wind farms, geothermal plants and hydroelectric plants. Initially, HDCs would purchase renewable electricity from the electricity market or directly from renewable power plants. Some have purposefully built their HDCs adjacent to renewable power plants to facilitate the sourcing of “green” energy. Over the past decade, HDCs in the US and Western Europe have even constructed solar farms and energy-storage systems as dedicated power plants for their facilities–with the grid providing back-up power.

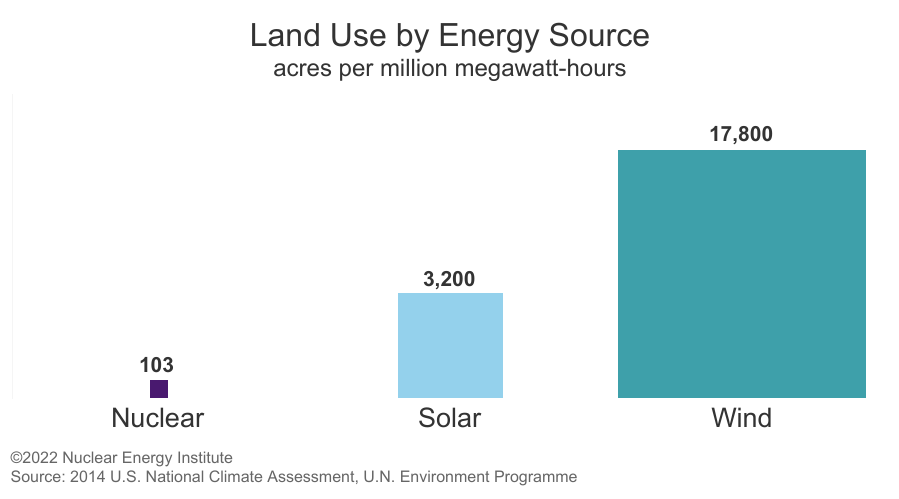

Due to (a) the large tracts of land required for a solar farm or large tracts of land or sea in the case of wind farms (refer to the graph below on Land Use by Energy Source), (b) the intermittent nature of electricity supply from solar and wind farms (i.e., solar farms generate electricity only when there is sunlight and wind farms generate electricity only when there is enough wind), (c) the relatively high cost of energy storage systems (typically paired with solar and wind farms) and (d) the ever-increasing and intensifying demand for HDCs in the next decade and beyond, HDCs have gravitated toward the other “green” source of electricity–a new generation of nuclear power plants, known as Small Modular Reactors or SMRs.

Smaller, Modular, Safer, Faster, Competitively-Priced Electricity and Green

These are the claims of a number of relatively new companies in the SMR sector, which will bear out in the course of the next several years as each of their respective first commercial plants are commissioned in the United States and, thereafter, similarly deployed or exported commercially to US-allied countries that have a receptive policy towards the civil use of nuclear energy.

Smaller

Prior to this new generation of SMRs, existing nuclear power plants in operation today are typically in the range of 1,000 MW or above; hence, the so-called large gigawatt-scale pressurized water reactors or legacy PWRs, the prevalent type of commercial reactor up to this time (2024). In contrast, SMR capacities range from 2-7 MW that can fit into cargo containers (Xe-Mobile) to 924 MW (77 MW x 12 modules, NuScale). Other examples of SMR capacities (this is NOT an exhaustive list) include:

80 MW scalable in “four pack” configuration to 320 MW–Xe-100

150 MW (2 x 75 MW configuration) and multiples of 150 MW–Kairos Power

345 MW (Natrium plant currently under construction)--TerraPower

308 MW (4 x 77 MW), 462 MW (6 x 77 MW), 924 MW (12 x 77 MW)--NuScale

Modular

Apart from Xe-Mobile, which is transportable and designed for quick deployment in military operations, disaster relief, critical infrastructure and remote micro-grid communities, the above examples indicate the modularity of design, which can be sized, configured and scheduled for commissioning to address the specific needs of the end-user. For example, a hyperscale data center (an end-user) could match its initial phase of computing capacity with the equivalent capacity of power generation. Thereafter, additional phases of computing capacity could likewise be paired with the equivalent additional capacity of power generation–instead of overbuilding the initial power supply with a single large reactor. The same phased approach to building additional capacity of power generation could be implemented with industrial and mixed-use estates as they are gradually populated by locators. Further, multiple modules within a single location minimize the need for backup power during refueling outages.

In the case of TerraPower’s Natrium plant, it has a baseload capacity of 345 MW plus an energy storage system (using molten salt) with the capability of ramping up to 500 MW for short periods (up to 5.5 hours)--a feature that is relevant for high-renewable penetration grids where variable power output requires balancing. For a better appreciation of TerraPower's Natrium plant, please refer to the article of Charles W. Forsberg dated 23 August 2021 entitled "Separating Nuclear Reactors from the Power Block with Heat Storage to Improve Economics with Dispatchable Heat and Electricity" which may be accessed by clicking the link.

Noteworthy is the last example in the above list (Helion), which is a nuclear FUSION plant–NOT a nuclear FISSION plant like the rest of the examples. Nuclear fusion is much more efficient than nuclear fission and, unlike nuclear fission, it does NOT produce long-lasting radioactive waste; hence, nuclear fusion is considered the holy grail of clean energy. Unfortunately, notwithstanding the press release of Helion, which suggests that a 50 MW nuclear fusion plant may be online by 2028, the consensus today, particularly among peers in the scientific community, is that nuclear fusion is still around one to two decades away from commercialization.

On the other hand, the rest of the examples above, which are nuclear fission plants, are targeting to commission their first commercial plants in the United States in 2 to 5 years–before 2030.

Proven Technology

Although these SMRs are a new generation of nuclear reactors, they are essentially refinements and innovations rooted in established and proven commercial technologies of numerous past nuclear fission plants that have operated successfully and safely throughout the world over the course of several decades.

Faster

The substantial reduction in size of SMRs allows the repeated fabrication of critical modules and components by highly trained workers at the point of origin (think mass production factory with economies of scale), thereby enhancing the quality control, the cost control and the time-to-delivery of the product. Further, upon delivery on site, such modules and components are mostly assembled (not fabricated), substantially reducing construction time.

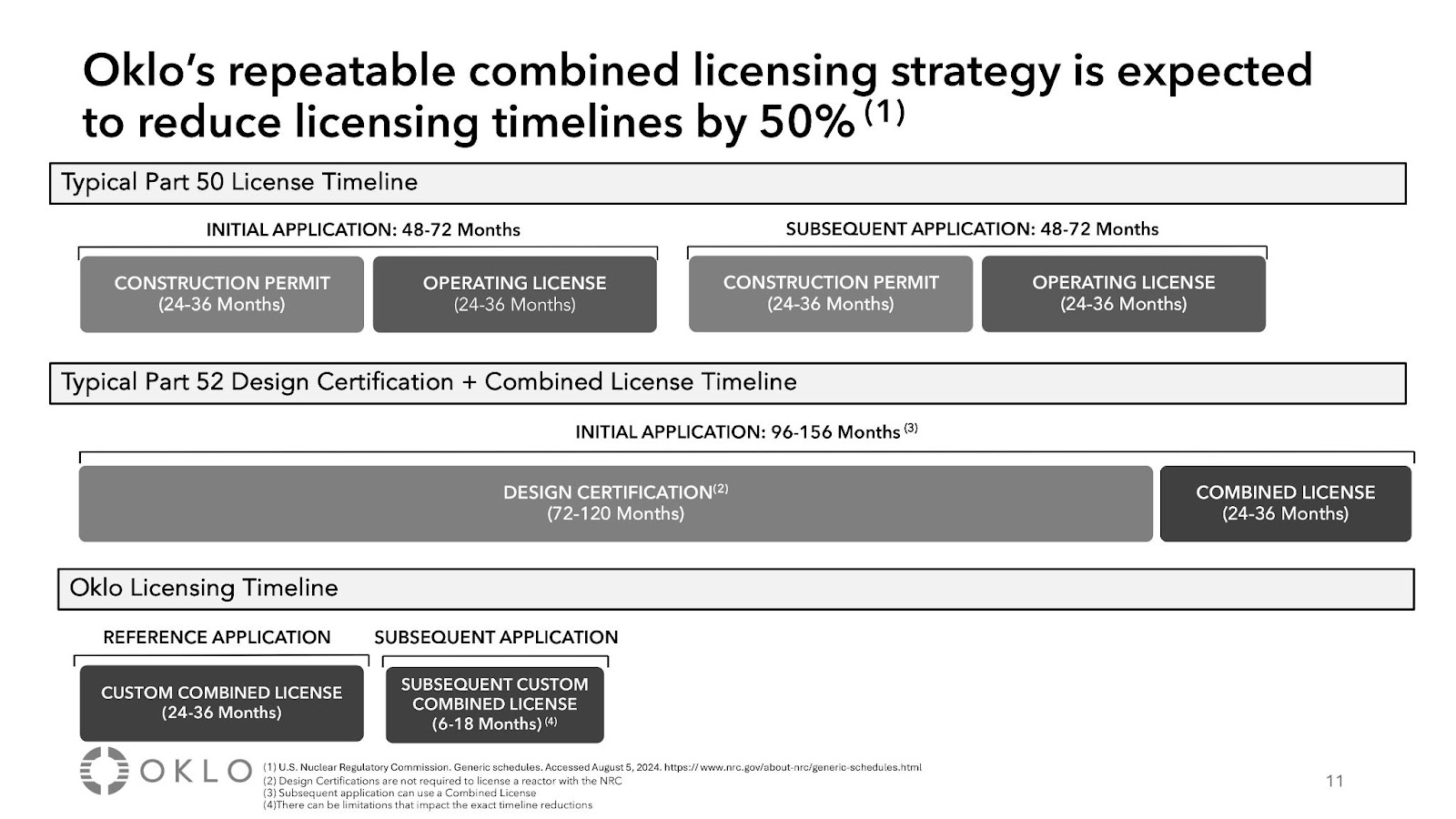

The permitting process of a nuclear plant with respect to nuclear regulatory agencies anywhere in the world is notoriously arduous and, at best, glacial in pace. That said, SMR companies like Oklo are also streamlining the regulatory and permitting process of SMRs in the United States (refer to the graph below on Oklo’s reduction of licensing timelines, page 11 of the 2Q 2024 company update of Oklo), which is expected to significantly reduce the time-to-delivery of commissioned SMRs and, therefore, be more responsive to the timing requirements of customers.

This streamlined permitting process of SMRs in the United States is itself a critical export component (i.e., there is no need to reinvent the wheel in other countries) that is just as valuable as the exported SMRs themselves, particularly for countries that are introducing nuclear energy into their energy mix but lack the experience in nuclear energy regulation, which inadvertently morphs into regulatory paralysis, corruption and, ultimately, nuclear power projects that never see the light of day.

Safer

Although there are several types of SMRs, the common thread among this new generation of reactors is the passive systems and inherent safety characteristics, such as low power and operating pressure. Passive systems rely on physical phenomena, such as natural circulation, convection, gravity and self-pressurization. This means that no human intervention or external power or force is required to shut down systems (which was NOT the case in Fukushima). These increased safety design features significantly lower or eliminate the potential for unsafe releases of radioactivity to the environment and the public in case of an accident.

In the case of Oklo*, the company has focused on the technology with the most demonstration history, with inherent safety, while having the capability to use waste as fuel. By far, liquid-metal-cooled, metal-fueled fast reactors have the most demonstration history of the advanced fission technologies at over 400 reactor-years of operating experience worldwide. The very first power plant to produce useful electrical power from fission was a liquid-metal-cooled, metal-fueled fast reactor – the Experimental Breeder Reactor-I (EBR-I). It's successor, the Experimental Breeder Reactor-II (EBR-II), operated for decades and showed that it could easily remain safe during challenges as severe as those that led to the Fukushima accident. The tests done with EBR-II showed that the coolant could be shut off and all shutdown systems removed, and the reactor would naturally stabilize and shut itself down without damage. EBR-II is the underlying proven and safe technology behind the new generation SMR of Oklo. (This paragaph was taken from the website of Oklo.)

*I should mention that I am not connected with Oklo in any way. I am not an employee of Oklo. I am not an agent of Oklo and I am not receiving any compensation from Oklo. I am using information provided by Oklo in the public domain (which, in my view, has been communicated skillfully and clearly) to convey concepts and examples of the subject matter for the benefit and understanding of the reader.

Competitively-Priced Electricity

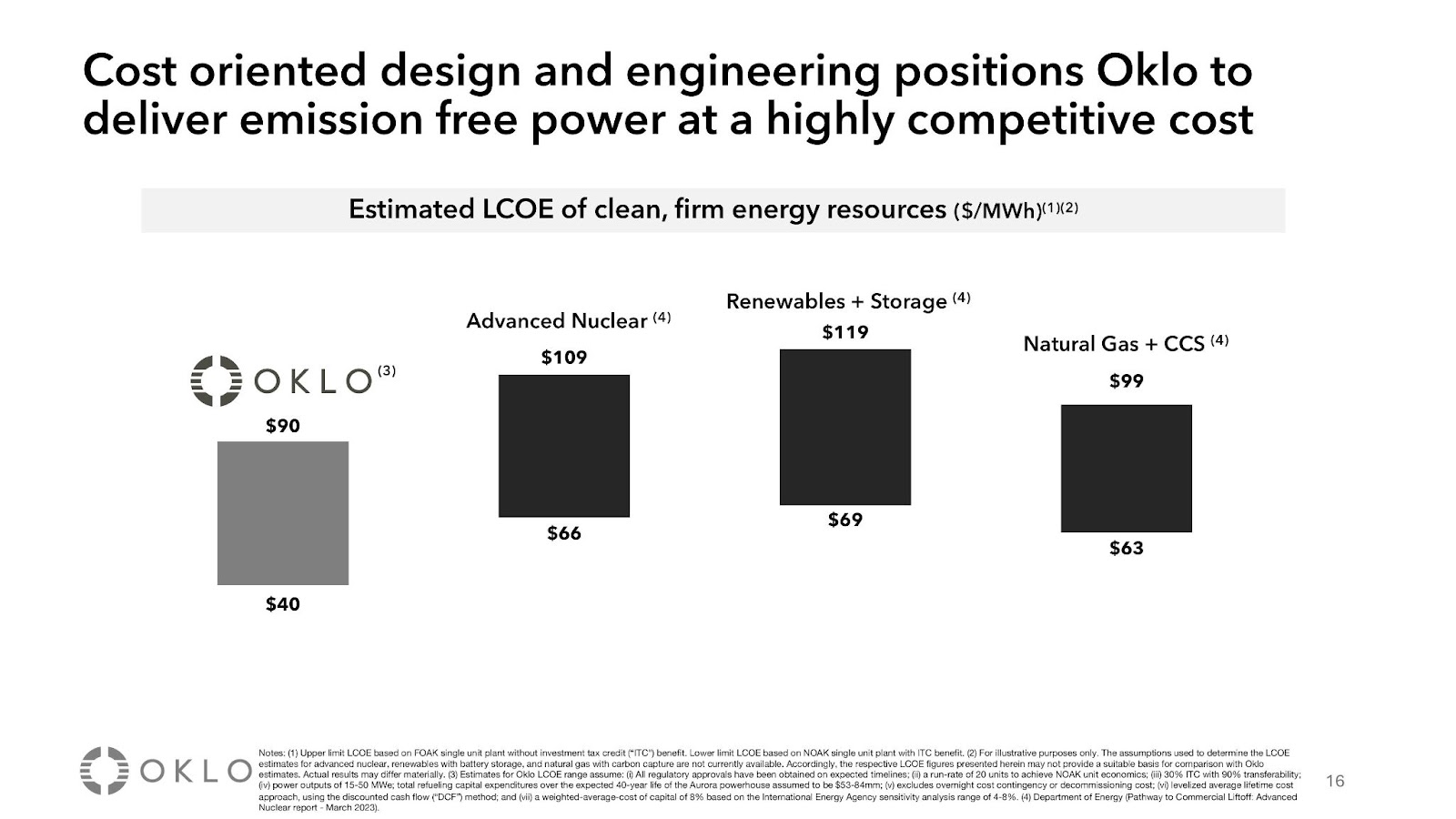

The following graph is an excerpt (page 16) from the 2Q 2024 company update of Oklo, which indicates a highly competitive LCOE (levelized cost of electricity) from an Oklo SMR. This will be verified after Oklo commissions its first commercial SMR in the United States.

The commercialization of the new generation of SMRs in the United States (like Oklo's) have been enabled by substantial subsidies from the US Federal Government. One example, which represents the tip of the iceberg, is the recent announcement by the Biden-Harris Administration to provide US$900 million in funding to support the initial domestic deployment of Generation III+ (Gen III+) small modular reactor (SMR) technologies. This, in addition to other subsidies from the US Federal Government, will usher the commercialization of these new generation of SMRs initially in the United States and eventually the exportation of the same to US-friendly countries--like the Philippines.

The Philippine is a developing economy that cannot afford to provide outright subsidies to SMR enterprises like the US Federal Government. However, the Philippine government has an existing "arsenal" of fiscal incentives that should be applied to the fullest extent (and more) to both SMR and HDC enterprises that locate in the country, much the same way these incentives have been applied to attract and develop certain strategic industries in the country.

For example, each of the SMR and HDC locators within a nuclear powered HDC complex contemplated in this strategy may avail of Philippine government fiscal incentives as PEZA registered enterprises. In addition, these fiscal incentives should be enhanced and bespoke to reinforce the Philippine government's commitment to this particular sector of nuclear powered HDCs. The following table contemplates some of these enhancements to the current fiscal incentives of PEZA registered enterprises.

In addition to the above enhancements of fiscal incentives, the development and implementation of a carbon credit system in the Philippines, which is still in its nascent stages, should be aggressively pursued by the Philippine government. These factors will contribute to the competitive price of electricity of SMRs in the Philippine market.

Senator Francis Escudero (Philippine Senator) has advocated the exemption of electricity sales from the value-added tax (VAT), currently at 12%. Considering electricity is one of the most basic commodities of society today and the fact that Philippine consumers have been paying for one of the highest rates of electricity in Asia, Senator Escudero’s proposal should have been legislated and implemented yesterday. That said, given the imperative to reduce greenhouse gas emissions, the VAT exemption could be applied only to the sales of electricity from renewable and green sources, like solar, wind, geothermal, hydroelectric and nuclear power installations, thereby enhancing the competitiveness of these facilities (relative to fossil fuel plants) and encouraging the market to develop more of the same going forward. This selective exemption of VAT on the electricity sales of renewable and green installations works together with the participation of the Philippines in a carbon credit system adhered to by the international community to reflect (appropriately, I should add) the true cost of electricity of green and fossil fuel plants vis-a-vis the immeasurable damage wrought by greenhouse gas emissions to the planet.

Green

Although NOT considered renewable energy, nuclear energy is referred to as a green energy technology as it produces nearly zero carbon dioxide or other greenhouse gas emissions. Nuclear energy also avoids producing air pollutants that are associated with burning fossil fuels for energy.

The Gorilla in the Room: Radioactive Waste

Because nuclear fusion, which does NOT produce long-lasting radioactive waste, is still around one to two decades away from commercialization, the new generation of SMRs (nuclear fission) remains a viable and rational green energy option in addition to renewable energy in the global effort to mitigate climate change. That said, SMRs generate radioactive waste, which are broadly classified as follows:

Spent Nuclear Fuel (SNF) or High Level Waste (HLW) and

Low and Intermediate Level Waste (LILW), which is further categorized as either

Short-Lived LILW or

Long-Lived LILW

In addition, innovations in the new generation of SMRs produce radioactive waste that differ from the radioactive waste produced by the large gigawatt-scale pressurized water reactors or legacy PWRs (the prevalent type of commercial reactor up to now) in terms of certain parameters, including:

energy-equivalent volume,

(radio-)chemistry,

decay heat, and

fissile isotope composition of (notional) high-, intermediate-, and low-level waste streams.

For a basic understanding of the differences in the radioactive waste produced by new generation SMRs and legacy PWRs, please read the research article published by the Proceedings of the National Academy of Sciences (PNAS) entitled “Nuclear waste from small modular reactors” by clicking on the link.

Hence, while all radioactive waste (whether it is produced by new generation SMRs or legacy PWRs and whatever its classification or category) require both (a) storage and (b) disposal, the storage and disposal protocols for radioactive waste produced by legacy PWRs will need to be revisited and, indeed, revised/refined to account for the differences in the radioactive waste produced by new generation SMRs.

For a basic understanding of radioactive waste storage and disposal, please read the publication of the International Atomic Energy Agency (IAEA) entitled “The Long Term Storage of Radioactive Waste: Safety and Sustainability” by clicking on the link.

For countries that do NOT have any legacy PWRs in operations today (2024) and are just introducing new generation SMRs into their energy mix (e.g., the Philippines), the opportunity exists to develop and enforce the most appropriate and current protocols, specifically for the storage and disposal of radioactive waste produced by SMRs. This will require the support and assistance of the companies exporting their SMRs and the US government, including the relevant nuclear regulatory agencies in the US.

The Philippine government has only recently re-established its policy to include nuclear energy into the energy mix of the country to the tune of 4,800 MW by 2050. Notwithstanding the existence of the Bataan Nuclear Power Plant, which was never loaded with fuel or operated and had been mothballed in 1986, the most probable and, indeed, rational nuclear energy scenario in the Philippines going forward is one comprised entirely of new generation SMRs. Hence, the Philippine government needs to back-up its commitment to nuclear energy with the requisite policies, regulations and protocols for the storage and disposal of radioactive waste produced by new generation SMRs, including the establishment of a geological/engineered disposal site in the country in which all radioactive waste would eventually be deposited permanently.

It is not enough that the Philippine government permits the operations of new generation SMRs in the country. It is imperative that the Philippine government has a clear path towards the establishment of a geological/engineered disposal site.

To date, Finland is the only country that has begun construction of a repository for the final disposal of spent nuclear fuel, also known as a deep Geological Disposal Facility or GDF. The ONKALO repository in Olkiluoto, Finland (see illustration below) will store spent fuel from nuclear power reactors in copper canisters. This GDF in Finland could potentially be the model of the GDF in the Philippines, which would serve as the permanent disposal facility of all high-level waste of SMRs in the country.

The geology of Olkiluoto's bedrock, which is predominantly comprised of magmatic mica gneiss, was a critical factor in its selection as a GDF site. The following generalized geologic map of the Central Philippines suggests that the extensive neogene metamorphics in the vicinity of Mount Halcon on the Island of Mindoro might qualify as a potential GDF site.

In the United States, the Waste Isolation Pilot Plant (WIPP) is the nation’s only repository for the disposal of transuranic waste generated by atomic energy defense activities. It is NOT used for the disposal of nuclear waste produced by nuclear power plants.

The United States has four commercial low-level nuclear waste (LLW) disposal facilities: (1) Barnwell, South Carolina; (2) Clive, Utah; (3) Richland, Washington; and (4) Andrews County, Texas.

To date, the United States does not have a long-term storage facility for high-level nuclear waste. Instead, high-level waste is stored near or on-site at active or deactivated reactors. This is considered a temporary solution until a long-term high-level nuclear waste facility is built, which has been delayed for decades. This is an example of what should NOT to happen in the Philippines.

Several countries have advanced plans for GDF, including Canada, United Kingdon, France and Sweden.

Not enough fuel for SMR's today

Like GDFs are playing "catch-up" to the rise of new generation SMRs, another critical component in the supply chain needs to be scaled-up to ensure enough fuel to power SMRs.

"The current fleet of nuclear reactors runs primarily on uranium fuel enriched up to 5% uranium-235 (U-235). High-assay low-enriched uranium (HALEU) is defined as uranium enriched to greater than 5% and less than 20% of the U-235 isotope. Applications for HALEU are today limited to research reactors and medical isotope production. However, HALEU will be needed for many advanced power reactor fuels, and more than half of the small modular reactor (SMR) designs in development.

HALEU is not yet widely available commercially. At present only Russia and China have the infrastructure to produce HALEU at scale. Centrus Energy, in the United States, began producing HALEU from a demonstration-scale cascade in October 2023.

HALEU can be produced with existing centrifuge technology but requires a specific nuclear fuel cycle infrastructure and the development of new or modified regulations and licensing regimes. Moreover, new or modified transport containers will be required for the movement of the large quantities of HALEU required for the deployment of SMRs and advanced reactors.

Establishing the supply chain to produce and deliver HALEU to customers will require significant capital investment. Governments will need to play a role initially until demand from the commercial market provides a sufficient signal to support private investment." World Nuclear Association on HALEU, 13 December 2023

In this regard, Oklo Inc. and Centrus Energy Corp. (“Centrus”) announced on 28 August 2023 a new Memorandum of Understanding (“MOU”) between the two companies to support the deployment of Oklo’s advanced fission powerhouses and advanced nuclear fuel production in Southern Ohio, making the region a critical hub for the future of the U.S. nuclear industry. This is an example of several public-private partnerships ((PPP) in which the US government is working with other private SMR companies, like TerraPower, NuScale Power, and X-energy, to scale-up the production capacity of HALEU. In addition, several countries involved in nuclear energy research, including the U.S., Canada, the U.K., France, and Japan, are collaborating on developing both the technology and infrastructure needed to scale-up HALEU production. The question remains as to whether or not the commercial production of HALEU will be in sync with the deployment of new generation SMRs in the US and the rest of the world.

Using Natrium's estimated fuel requirements of 6 metric tons per gigawatt-year (t/GWe-y) of 16.5% Enriched Uranium Product (i.e., HALEU), the initial 4.8 GW (5.3 GW with load balancing capacity) of nuclear power contemplated in the Philippines would require approximately 1,000 metric tons of HALEU for the first 30 years of operations or 2,000 metric tons for the entire 60-year lifecycle of this entire batch of SMRs in the country--which is likely to represent a rounding error in the global supply of HALEU when it is produced commercially for the market.

A Nuclear Powered Hyperscale Data Center Complex in the Philippines

Philippines Commits to Nuclear Energy and Cooperates with USA

The Philippine government’s recent (September 2024) announcement to re-establish its policy to include nuclear energy into the energy mix of the country to the tune of 4,800 MW by 2050 is a significant milestone that enhances the country’s “toolbox” in mitigating climate change, particularly in the context of (a) replacing existing fossil fuel plants with green power plants AND (b) adding new green capacity to fulfill the demands of a growing economy.

The impetus for this energy policy direction was the signing of the United States-Philippines Civil Nuclear Cooperation Agreement in July 2023; therefore, the Philippines can reasonably expect to be working closely with US companies and the US government on the deployment of new generation SMRs in the country in the foreseeable future.

Highest-Value Utilization of Nuclear Energy and HDCs

4,800 MW of SMRs by 2050 appears to be prudent on a couple of fronts:

Although modest in scale, it may be enough to attract investments in new generation SMRs in the country.

The same modest scale limits the “baggage” associated with the storage and disposal of radioactive waste.

"A UK study suggests that with sufficient deployment —around 5 GW of SMR capacity— LCOE could reach parity with larger nuclear plants, assuming production of 10 SMR units annually." IAEA publication entitled "Advances in SMR Developments," 2024. As such, the Philippine government's decision to include an initial 4,800 MW or 4.8 GW of nuclear energy in the energy mix of the country appears to be at the threshold that would enable SMR's to supply electricity within an acceptable price range.

Because of its modest scale and the issue of radioactive waste, said 4,800 MW of nuclear energy constitutes a “silver bullet”--a limited resource that warrants a thoughtful and astute deployment strategy which would optimize the positive impacts on the economy, particularly in conjunction with the deployment of the abundant yet relatively untapped solar and wind resources in the country.

In an article published by Ecosystem (a research and advisory firm) entitled “The Next Frontier: Southeast Asia’s Data Centre Evolution,” the Philippines is not even mentioned among the notable regional data center hubs, which were Singapore, Malaysia, Indonesia and Thailand. Similarly, in the following graph of “Top 10 Emerging Global Data Center Markets, 2023,” the Philippines is absent.

|

Top 10 Emerging Global Data Center Markets, 2023

Source: Savills Industrial Whitepaper

Considering the business process outsourcing (BPO) industry, which employs about 1.7 million individuals and is a major contributor to the Philippine economy (with an estimated revenue of US$38 billion in 2024*), is imminently threatened by massive job losses due to the increasing adoption of AI technologies (which is enabled by HDCs), the government needs to work harder and smarter in building the position of the Philippines as an international telecommunications/HDC hub in Asia Pacific–if only to offset the decline and corresponding economic losses in the BPO industry.

*This is comparable to the full-year level US$37.2 billion personal remittances from overseas Filipinos in 2023 and the the country's total exports in the electronics manufacturing sector, which amounted to US$41.91 billion in 2023.

Mark Zuckerberg himself confirmed that energy constraints have become the largest bottleneck to building out HDCs. Hence, one potential strategy that would provide the competitive edge to the Philippines in the fast-growing and highly-competitive global industry of HDCs involves the integration of new generation SMRs with HDCs. This is consistent with the “bring your own power” or BYOP trend currently pursued by HDCs and will enable the Philippines to realize the highest-value use of its nuclear energy program while, at the same time, attract a critical mass of major players in the global HDC sector to locate in the country.

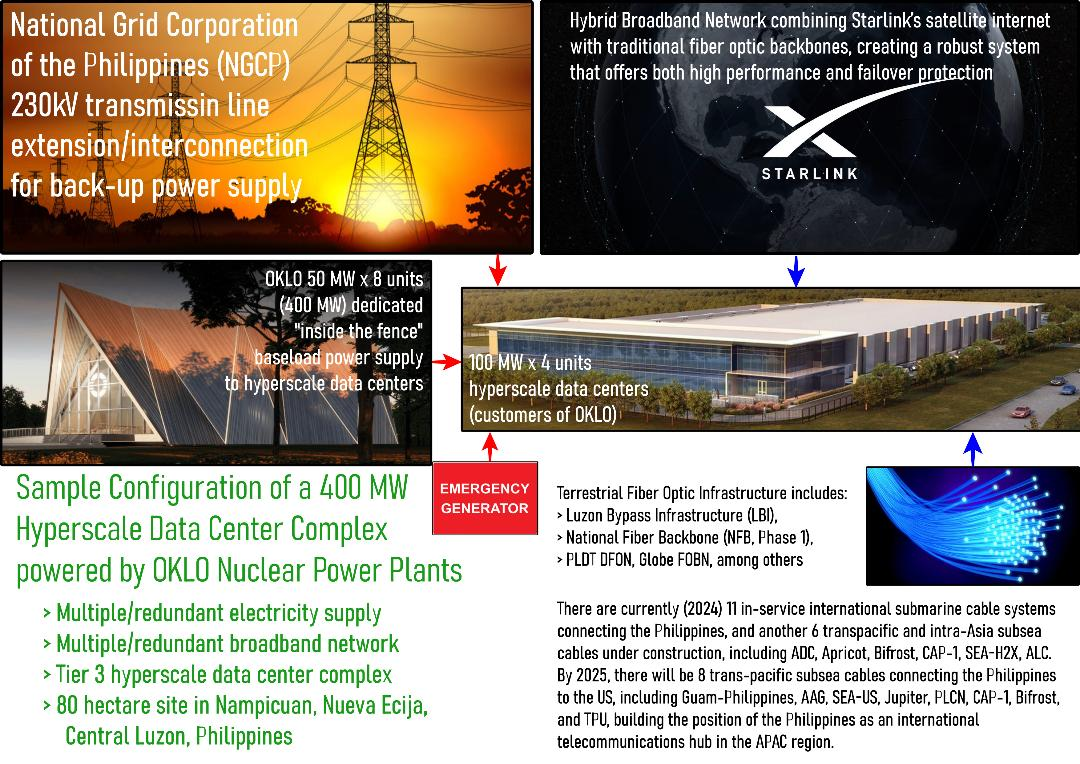

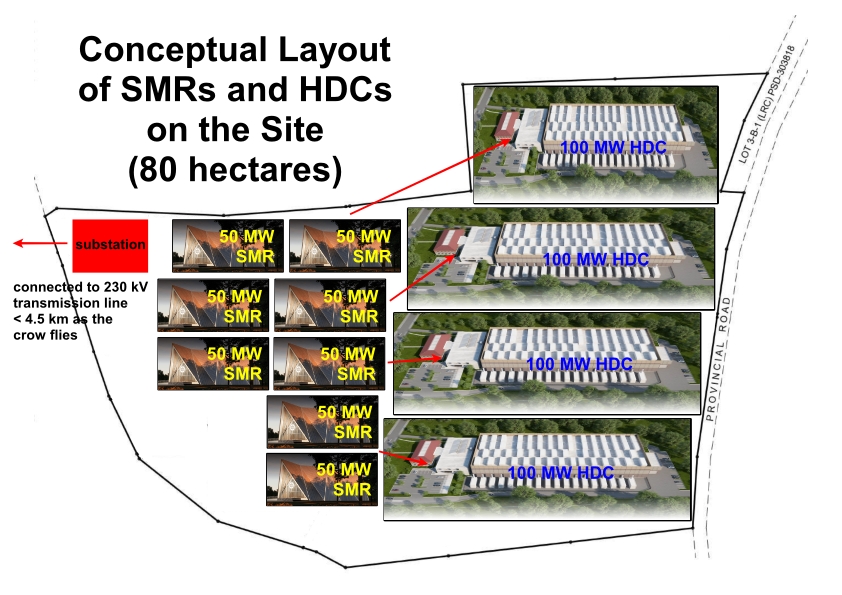

Sample Configuration of a 400 MW Nuclear Powered HDC Complex in the Philippines

The preceding illustration is based on the following:

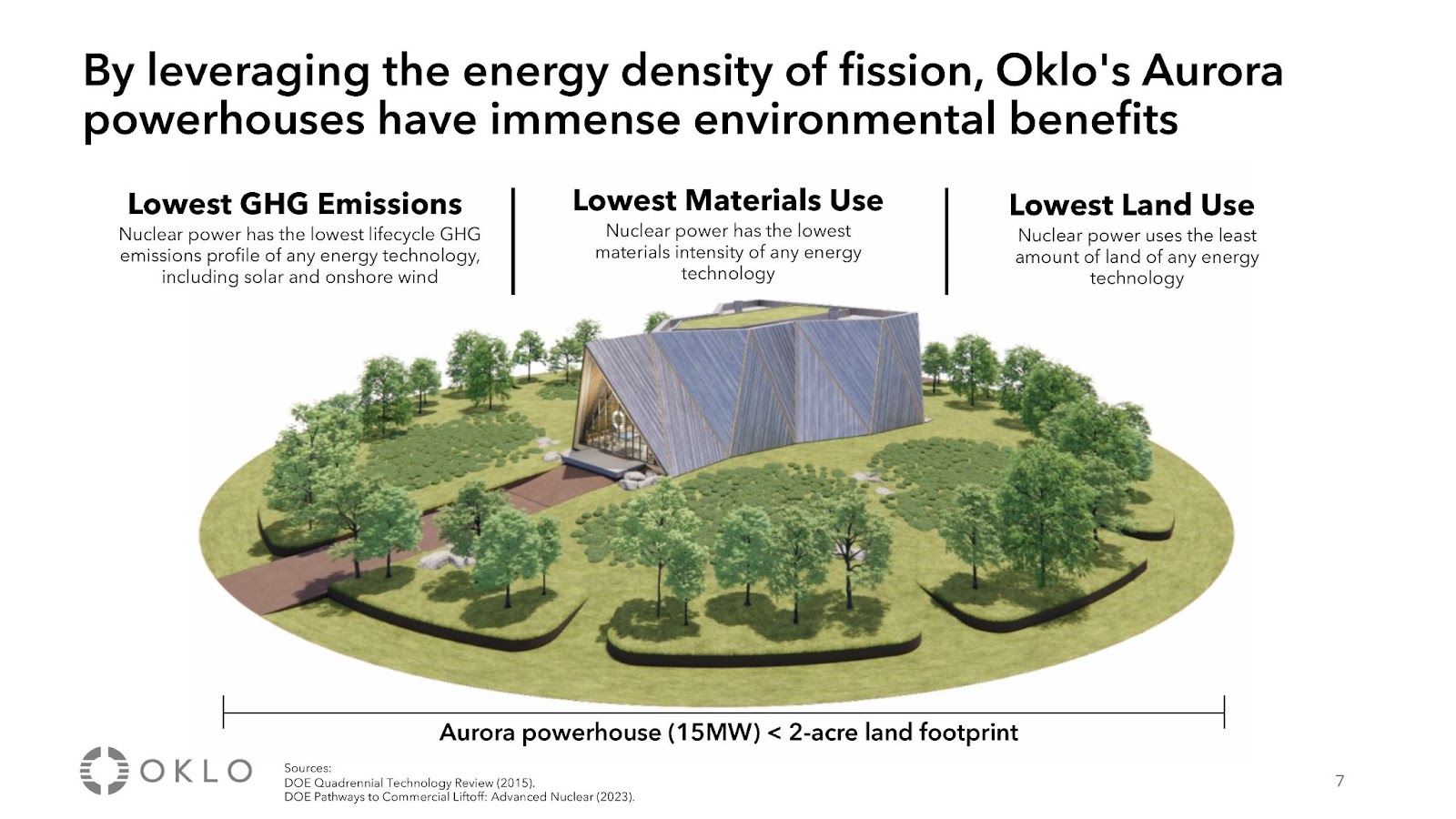

Oklo’s SMRs, which require 2 acres per 15 MW module (see the illustration below, page 7 of the 2Q 2024 company update of Oklo); hence, 400 MW of Oklo’s SMRs would require approximately 54 acres or 22 hectares;

2 acres per 15 MW module or 22 hectares for 400 MW of Oklo’s SMRs

An indicative standard footprint of 10 acres per 40 MW HDC; hence, a 400 MW (4 x 100 MW) HDC complex would require approximately 100 acres or 40.5 hectares;

For baseload power, each 100 MW HDC paired with 100 MW baseload nuclear power plant (2 x 50 MW SMR);

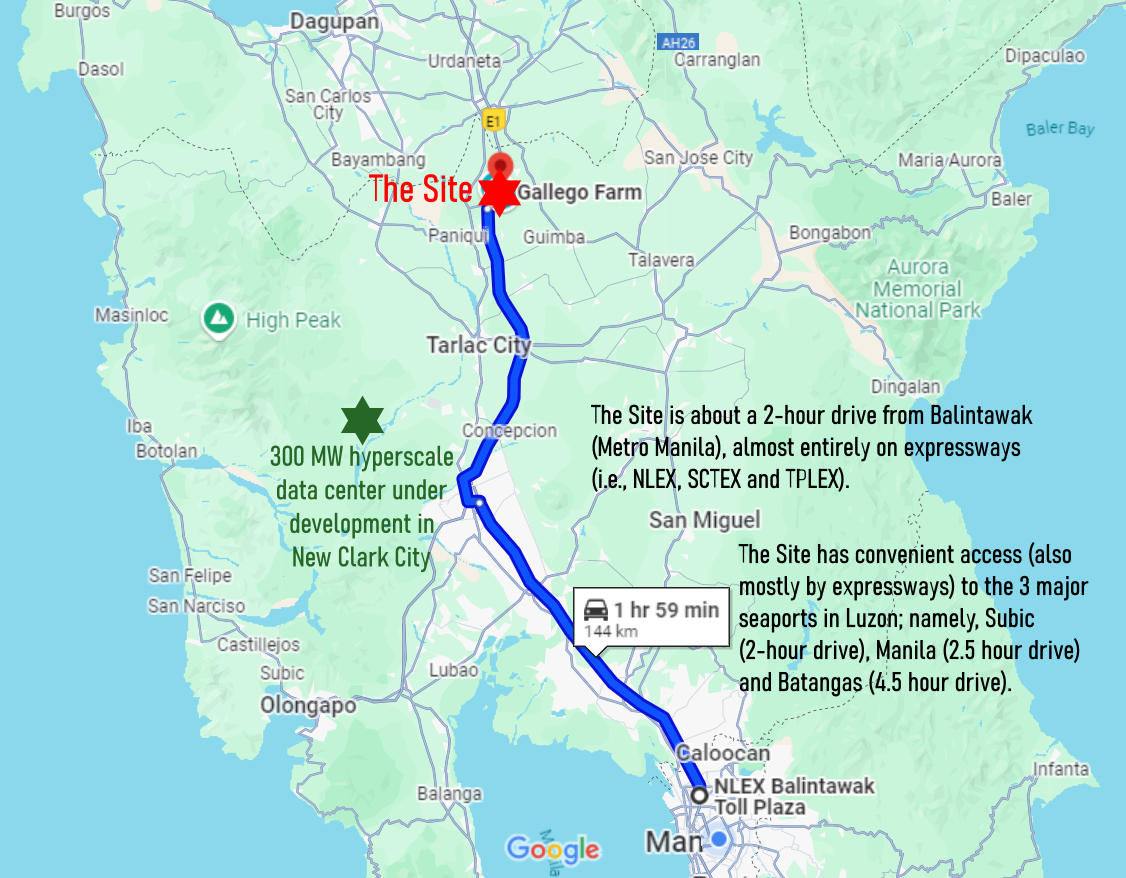

For back-up power, interconnection with 230 kV transmission line of the National Grid Corporation of the Philippines (NGCP) less than 4.5 km from the Site as the crow flies;

For emergency power, diesel-fueled power generator per HDC;

A privately-owned cattle ranch with an area of 80 hectares located in Nampicuan, Nueva Ecija, Philippines (the “Site”)--see conceptual layout of HDCs paired with their respective SMRs below;

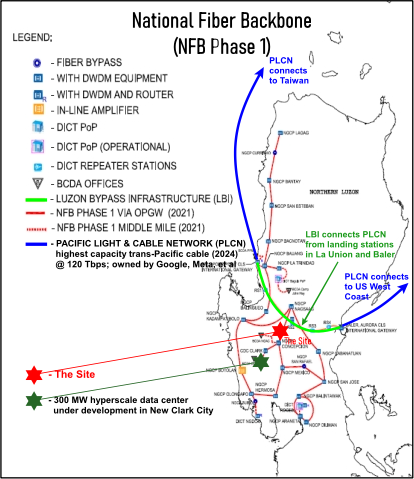

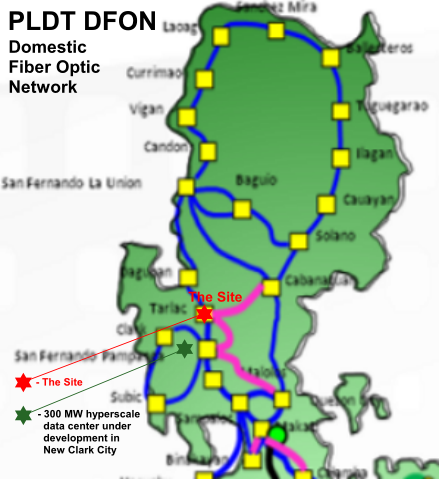

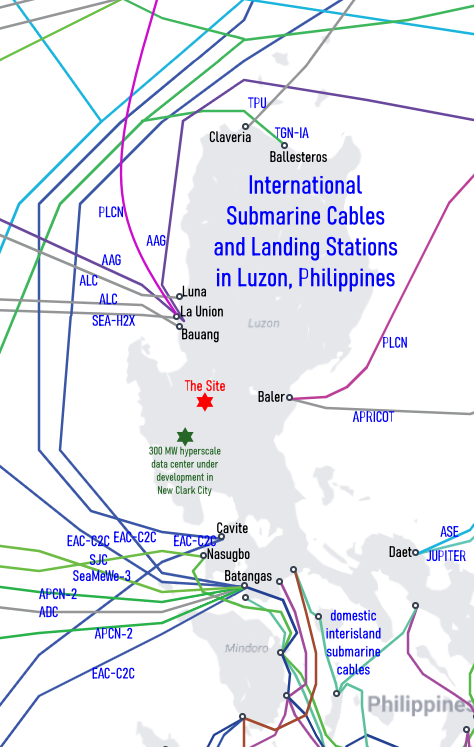

For fiber optic infrastructure in the vicinity of the Site, several terrestrial fiber optic backbones (i.e., Luzon Bypass Infrastructure, National Fiber Backbone (NFB Phase 1), PLDT DFON and Globe FONB) integrated with various international submarine cable systems; for high performance and failover protection, the option of a hybrid broadband network combining Starlink’s satellite internet with fiber optic backbones.

The following illustrations show the fiber optic infrastructure in the vicinity of the Site. Note the 300 MW HDC under development in New Clark City (located southwest of the Site), which was recently announced.

National Fiber Backbone (NFB Phase 1)

Note the Luzon Byass Infrastructure (LBI) that connects PLCN

from the landing stations in La Union and Baler.

International Submarine Cables and Landing Stations in Luzon, Philippines

(integrated with the terrestrial fiber optic backbones in previous illustrations)

The Strategy: Highest-Value Deployment of Nuclear Energy in the Philippines

BYOP Integration of SMRs with HDCs and Industrial/Mixed-Use Estates

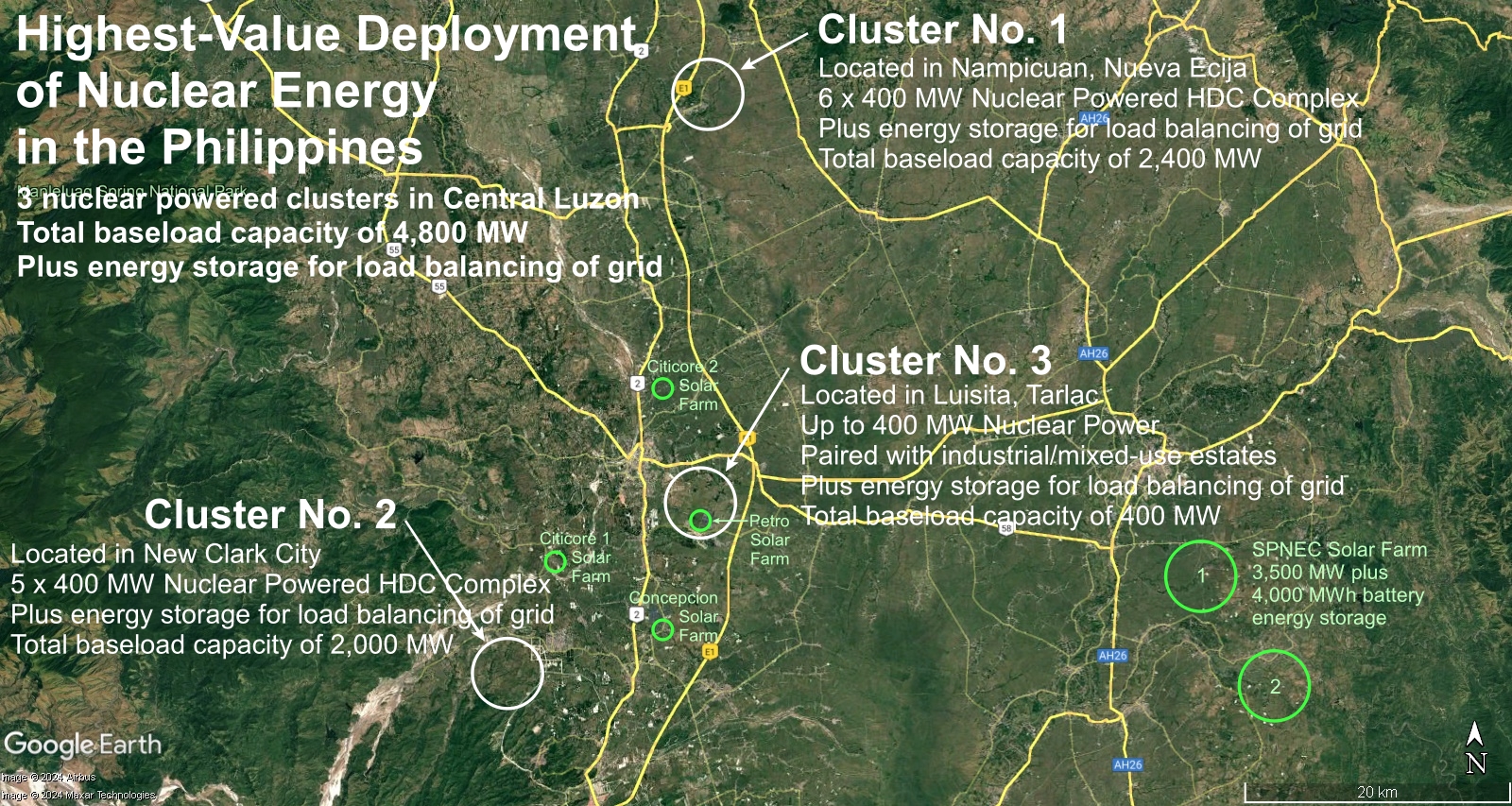

The foregoing discussion suggests that the Site, with multiple/redundant provisions of electricity supply and broadband access, could be the location of the first nuclear powered Tier 3 HDC complex in the Philippines AND potentially the genesis of several similar complexes in the vicinity of the Site (Cluster No. 1), thereby laying out the first component (BYOP) in the overall strategy of highest-value use of nuclear energy in the Philippines in conjunction with attracting a critical mass of HDCs in the country.

In addition to Cluster No. 1, a second cluster of nuclear powered HDC complexes can likewise be established in New Clark City (Cluster No. 2). The development of a 300 MW HDC in New Clark City (the largest HDC in the Philippines to date) could serve as the first customer in Cluster No. 2 with several similar complexes to follow in the vicinity of New Clark City.

Like New Clark City, the area of Luisita, Tarlac (also in Central Luzon between the vicinities of Cluster No. 1 and Cluster No. 2) is currently experiencing tremendous growth with the development of industrial and mixed-use estates by first tier conglomerates, which are also active developers, owners and operators of green energy facilities in the country. These include Cresendo of Ayala (290 hectares) and Tari of Aboitiz (200 hectares) in partnership with the Yuchengco Group (184 hectares), representing a core development of nearly 700 hectares–to be followed predictably by a bandwagon of other real estate developers.

The substantial demand for electricity in these estates will justify a phased build-out of baseload capacity, which is especially suited for SMRs. Over the course of the next decade, the baseload demand within these estates alone will likely reach several hundred megawatts, representing a smaller Cluster No. 3.

Central Luzon has the highest concentration of solar farms in the Philippines today and in the foreseeable future. The largest one called Terra Solar is currently being constructed by SP New Energy Corporation (SPNEC). Upon completion in 2 to 4 years, Terra Solar will have an installed capacity of 3,500 MW plus 4,000 MWh of battery storage. At night, the solar farm component of Terra Solar will not be generating electricity and, under one of many operational scenarios, the battery storage component can fulfill 400 MW of demand over a period of 10 hours (i.e., while there is no sunlight). Notwithstanding, like most grids all over the world increasing the percentage of renewable energy in their energy mix, the corresponding deployment of energy storage (particularly battery storage, which is relatively expensive) falls short of fulfilling demand during the intermittent periods that renewable energy plants are unable to generate electricity. In most cases, solar and wind farms do not even include a battery storage component as it typically dilutes the economic viability of these projects.

Nuclear power plants, including SMRs, are particularly suited and operate most efficiently as baseload plants, which is why they are best paired with HDCs that have fairly constant demand profiles 24/7, 365 days, year after year. That said, with some compromise in efficiency, SMRs, which function primarily as baseload plants, can be configured to also operate with non-battery energy storage systems and, as a result, can function both as a baseload plant and as a load balancing plant–particularly in grids with a high penetration of renewable energy and intermittent power output is a concern–in this case, the Luzon grid with the highest concentration of solar farms and a shortage of energy-storage systems.

Terra Power of Bill Gates (not to be confused with Terra Solar of SPNEC) is currently constructing Natrium, the first new generation SMR that functions both as a baseload plant and as a load balancing plant. Natrium is equipped with a molten salt energy storage system, which is reportedly more resilient, flexible and cost-effective than current grid-scale battery storage technology.

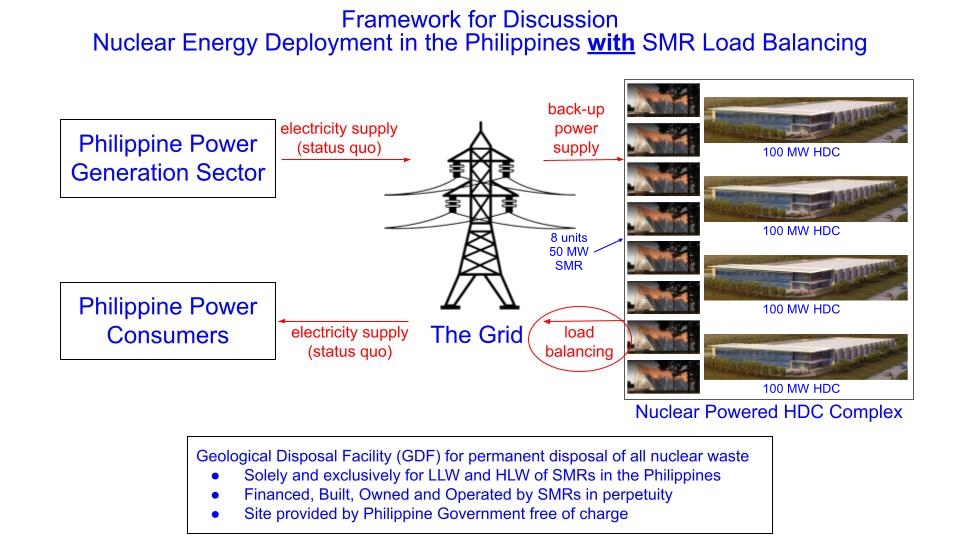

Load Balancing of Grid with SMRs

Balancing the load of the grid with SMRs configured with energy storage systems constitutes the corollary/second component (Load Balancing) of the overall strategy of highest-value use of nuclear energy in the Philippines in conjunction with attracting a critical mass of HDCs in the country. This corollary does NOT entail building additional SMRs contemplated in Cluster Nos. 1, 2 and 3 in the preceding discussion. It does entail configuring the same SMRs in said clusters with energy storage systems (similar to the Natrium plant) that will fulfill, first, the baseload requirements of HDCs/industrial mixed-used estates and, second, the load balancing requirements of the grid. Hence, it becomes another integral part of the country’s efforts to mitigate climate change, which works in combination with renewable energy and other energy storage systems.

Unlike many of the energy storage systems in the market today (battery energy storage systems being one of many that can be installed on a stand-alone basis with or without a corresponding power plant, renewable or otherwise), the energy storage system of an SMR (similar to the Natrium plant) is NOT a stand-alone system but works only in conjunction with an SMR; therefore, it has to be planned and executed from the outset alongside the development and construction of the SMR. It cannot be an afterthought. Consequently, if this second component (Load Balancing) of the overall strategy is to be pursued properly, the SMRs primarily intended to supply baseload power to HDCs should be properly sized and configured to also provide load balancing to the grid.

Not to be taken lightly in this strategy, the Philippine government and the National Grid Corporation of the Philippines (NGCP) should ensure that the required extensions and upgrades to the grid (i.e., transmission lines, substations, among other things) are expeditiously addressed not only in the context of providing back-up power to SMRs paired with HDCs and industrial/mixed used estates but also in providing adequate transmission capacity to enable the same SMRs to export power for balancing the load of the grid. Because the contemplated clusters of SMRs in this strategy are within a limited geographical area in Central Luzon, said grid infrastructure extensions and upgrades should be manageable and even enhance the efficiency and reliability of the grid.

Commence Permitting Yesterday

Because permitting a hyperscale data center is less arduous than permitting a nuclear power plant (probably anywhere in the world), permitting the Site for the development of a nuclear powered HDC complex, particularly with respect to the installation of SMRs, should be accomplished well ahead of time (as in several years ahead of time) with the relevant Philippine government authorities, culminating in the issuance of a development permit for the SMR enterprise locating on the Site. As such, when the SMR enterprise has secured the commitment of its first HDC customer to locate on the Site and jointly execute the requisite Power Purchase Agreement (PPA), the SMR enterprise’s milestones of financial closing up to commissiong of the nuclear power plant would coincide with the construction and commissioning of the HDC (i.e., unencumbered by delays in the government permitting process of a nuclear power plant, which would have been mostly accomplished ahead of time).

Noteworthy is the landmark legislation in the United States, known as the ADVANCE Act of 2024, which, among other things, directs the United States Nuclear Regulatory Commission (USNRC) to consider novel methods of licensing small reactors with unique safety characteristics resulting in shorter licensing timelines. It would behoove the Philippine government to legislate a similar law to ensure the prompt and cost-efficient licensing/permitting of SMRs in the country.

Sidebar on Nuclear Power in France

“As of December 2023, according to data from Ember and the Energy Institute as processed by Our World in Data, France generates roughly two-thirds of its electricity from nuclear power, well above the global average of just under 10%. This heavy reliance on nuclear energy allows France to have one of the lowest carbon dioxide emissions per unit of electricity in the world at 85 grams of CO2 per kilowatt-hour, compared to the global average of 438 grams.” (Wikipedia, nuclear power in France)

Nuclear power accidents in France[107][108]

In July 2008, 18,000 litres (4,755 gallons) of uranium solution containing natural uranium were accidentally released from Tricastin Nuclear Power Centre. Due to cleaning and repair work the containment system for a uranium solution holding tank was not functional when the tank filled. The inflow exceeded the tank's capacity and 30 cubic metres of uranium solution leaked, with 18 cubic metres spilled on the ground. Testing found elevated uranium levels in the nearby Gaffière and Lauzon rivers. The liquid that escaped to the ground contained about 75 kg of natural uranium, which is toxic as a heavy metal, but only slightly radioactive. Estimates for the releases were initially higher, up to 360 kg of natural uranium, but revised downward later.[111] French authorities banned the use of water from the Gaffière and Lauzon for drinking and watering of crops for 2 weeks. Swimming, water sports and fishing were also banned. This incident has been classified as Level 1 (anomaly) on the International Nuclear Event Scale.[112] Shortly after the first incident, approximately 100 employees were exposed to minor doses of radiation (1/40 of the annual limit) due to a piping failure.[113]

In October 2017, EDF announced it would repair fire safety system pipes at 20 nuclear reactors to increase seismic safety after discovering thinning metal in some sections of pipes. EDF classified this as a Level 2 (incident) on the International Nuclear Event Scale.[114]

The above table and descriptions of nuclear power accidents in France were copied entirely from Wikipedia, nuclear power in France.

Like all industrial enterprises, nuclear power plants in France (and in the rest of the world) have incidents, accidents and fatalities. That said, nuclear power plants have the unenviable distinction of the risk of radiation exposure, albeit in varying degrees.

The most well-known nuclear power plant accidents occurred at Three Mile Island (USA, 1979), Chernobyl (Ukraine, 1986), and Fukushima (Japan, 2011). All of these accidents involved the release of radioactive material and initiated radiological emergency management efforts. These accidents were highly publicized worldwide and rightfully so. However, such notoriety also created a strong bias in public opinion against the nuclear power industry in spite of its long history (more than half a century) of mostly successful and safe operations (really). Not every accident in nuclear power plants results in public radiation exposure. Even serious accidents could occur without public exposure. And even in the event of public radiation exposure, which is an ever-present risk in a nuclear power plant, these occur at varying degrees, which are rarely catastrophic and can be mitigated most of the time.

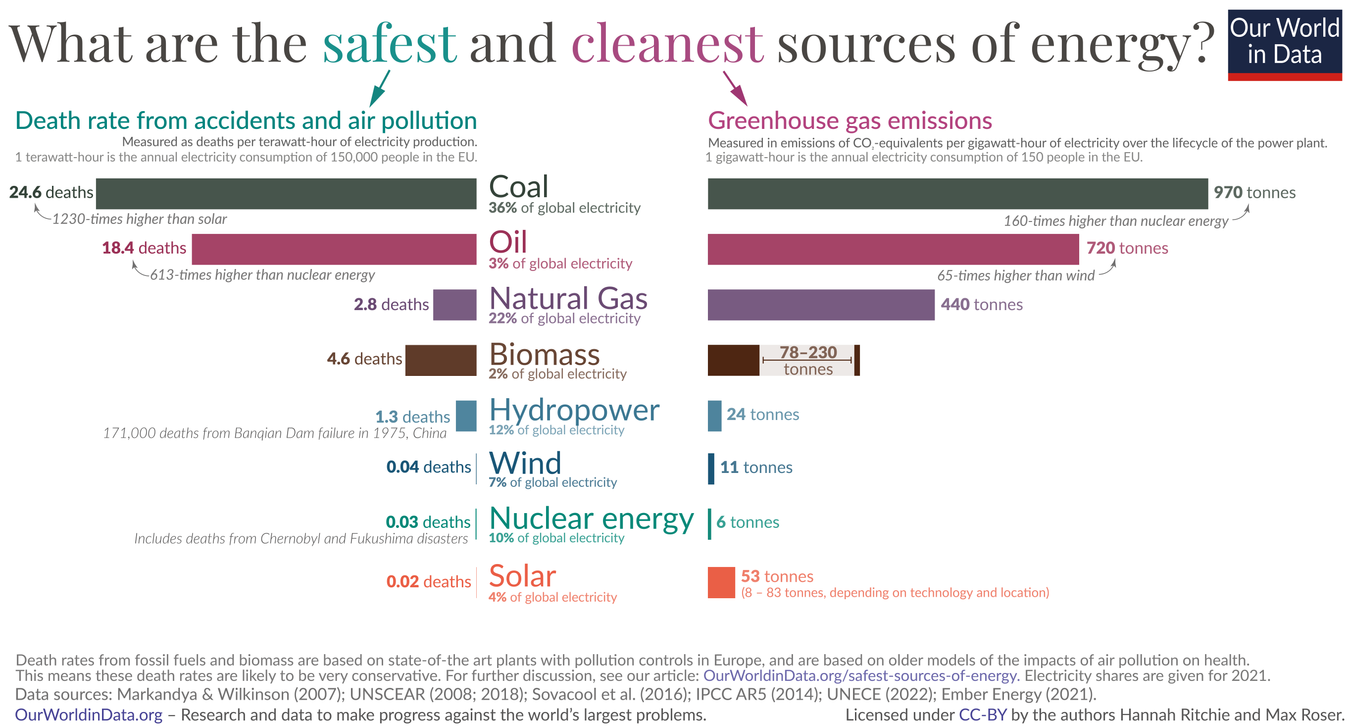

The following graph published by Our World in Data is a sober representation of the safety record of nuclear energy compared to other modes of power generation.

“In the November 2023 COP28 climate conference in Dubai, French President Emmanuel Macron triumphantly declared that “nuclear energy is back”. His celebratory remark was uttered after France led a group of 20 countries in signing a pledge to “triple nuclear energy capacity from 2020 by 2050”. Also in November 2023, the European Parliament backed the development of small modular reactors (SMRs), a versatile technology that many consider to be the future of the industry. Two months later, Energy Transition Minister Agnes Pannier-Runacher said that France will need to build 14 new nuclear power plants rather than the six currently planned if the country is to meet its energy transition goals.” (Future Power Technology, February 2024)

The question at hand is, do the benefits outweigh the risks? In the case of France, the answer appears to be a resounding “Yes!” The question also appears to have been answered by the Philippine government’s decision to include nuclear energy in the energy mix of the country.

Due to the exigencies of climate change and considering all of the commercially available solutions today, I would agree with this policy decision as part of a realistic approach to address climate change, PROVIDED that all SMRs in the Philippines are built, owned and operated by reputable (competent, professional, high-integrity) private sector enterprises.

For example, regardless of its condition even if it was brand-spanking new, the Bataan Nuclear Power Plant being operated by the National Power Corporation (NPC, a Philippine Government Owned and Controlled Corporation that exemplified the worst in government incompetence and corruption and, therefore, was eventually dissolved (mostly) with the passage of EPIRA in 2001) would have been a catastrophic disaster waiting to happen.

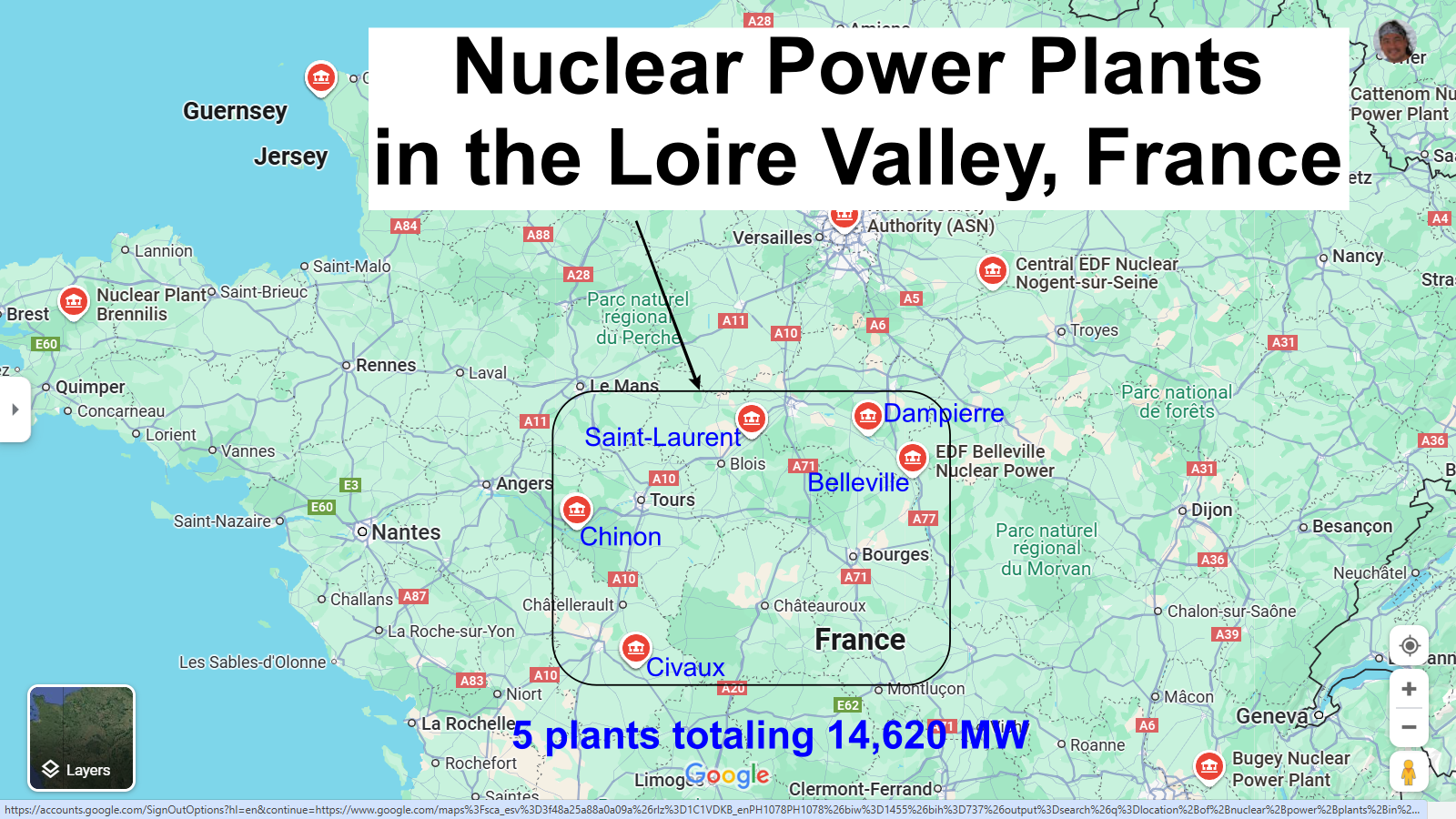

One of my most memorable trips abroad was a visit to the Loire Valley of France, rich in history, culture and wonderful French provincial cuisine. It is also an agricultural region famous for its wines, among other gastronomical delights. While touring the region and visiting various historic castles and chateaus, I happened to come across a nuclear power plant, which was surprisingly unobtrusive. I actually needed to probe the surroundings and road signages to realize that I was driving along the fenceline of the power plant. The neighboring properties and farms appeared undisturbed and just as idyllic as the rest of the rural areas I visited in the Loire Valley.

The following is a map of a portion of France highlighting the region of the Loire Valley in which several nuclear power plants are located; namely,

Civaux Nuclear Power Plant; 1,495 MW x 2 units = 2,990 MW

Chinon Nuclear Power Plant; 905 MW x 4 units = 3,620 MW

Saint-Laurent Nuclear Power Plant; 915 MW x 2 units = 1,830 MW

Dampierre Nuclear Power Plant; 890 MW x 4 units = 3,560 MW

Belleville Nuclear Power Plant; 1,310 MW x 2 units = 2,620 MW

TOTAL = 14,620 MW

Conclusion

Similar to the Loire Valley (with 14,620 MW) but "master planned" to accommodate only one-third of the generating capacity, Central Luzon (proposed 4,800 MW) is featured in the following illustration, which encapsulates the overall strategy of BYOP (Bring Your Own Power) highest-value deployment of nuclear energy in the Philippines, including pairing SMRs with HDCs within nuclear powered HDC complexes (Cluster Nos. 1 and 2), pairing SMRs with industrial/mixed-use estates (Cluster No. 3) and configuring the same SMRs (in Cluster Nos. 1, 2 and 3) with energy storage systems to provide load balancing to the grid.

The BYOP component of this strategy (i.e., SMRs supplying baseload power to HDCs) addresses the bulk of the high-demand and high-reliability electricity requirements of HDCs. Thanks to the clever business structure deviced by the HDC sector with SMR companies that are jointly poised to make this happen in the United States.

To transplant this winning economic model on our shores, there remains the overarching challenge for the Philippine government and the Philippine conglomerates that dominate the power sector and the fiber optic infrastructure in the country, which is to ensure the adequacy at all times of:

- power supply and reserves to provide redundant/back-up power to the massive influx of Tier 3 HDCs;

- transmission interconnections and capacity to exploit the grid load balancing provided by SMRs; and

- fiber optic infrastructure (terrestrial backbones, submarine cables, landing stations and the integration thereof) to provide the redundant broadband connectivity and capacity for the massive computing capacity of Philippine-based HDCs to service the global market.

Are we, the Philippines, ready for the challenge?

Postscript

As of 2023, the total installed capacity of coal power plants in the Philippines was 12,400 MW, which is 44% of the 28,300 MW total installed capacity of power generation in the country. In the Argus news article dated 20 June 2024 entitled "Philippines keeps adding coal-fired power capacity," the Philippines' Department of Energy (DOE) expects an additional 2.255GW of coal-fired power generation capacity to come on line by 2028, meaning the country will still be reliant on coal despite its decarbonisation plans.

At some point after the 20 to 30 year life-cycle of each of these coal plants (2040 and beyond), approximately 15,000 MW (15 GW) will need to be replaced one decommissioned coal power plant at a time by power generation technology that does not emit greenhouse gases. SMR's are particularly suited for this gradual replacemnt of coal capacity in the Philippines. SMRs can be built on the exact same sites of these decommissioned coal plants (with plenty of area to spare for future expansions) and continue to use the existing transmission interconnection facilities on each site to supply power to the grid. In fact, because the transmission grid is also being used for the country's fiber optic backbone, the large footprint of these decommissioned coal plants (relative to the small footprint required by SMRs) would be suited for a much larger roll-out of (15,000 MW) nuclear powered HDCs in the long run, provided, of course, that the said fiber optic backbone is substantially built-up to handle the massive broadband capacity and redundancies required by HDCs.

If the Philippines executes the foregoing strategy of nuclear powered HDCs in the near term, then it would be far better equipped to undertake the more audacious program of replacing 15,000 MW of coal capacity with SMRs in the long run.

Breaking Free from Coal: How SMR Technology Can Be a Solution in Securing ASEAN's Energy Independence. In this article, the UK's approach to phasing out coal begs to be emulated by the Philippine power generation sector. The following paragraphs are excerpts from this article.

"In 2015, the UK became the first country to pledge to completely stop using coal power by 2025. The United Kingdom has made significant progress in reducing its reliance on coal-fired power over the past decade. Coal once supplied nearly 40% of the UK's electricity in 2015, but by 2022 accounted for just 1.5%. This decline is the result of deliberate policy actions by the UK government to drive coal off the energy system." Phasing out coal has been and continues to be essential for the UK to meet its target of net-zero emissions by 2050.

"A major driver of coal's decline has been the UK's carbon price support mechanism, introduced in 2013. By putting a price on carbon emissions, it has made coal generation economically uncompetitive compared to lower carbon alternatives like natural gas and renewables. The UK has also legislated a phase-out of unabated coal generation by 2025, forcing closure of coal plants."

"In 2023, the UK government launched the Great British Nuclear (GBN) initiative. GBN aims to rapidly expand nuclear power generation in the UK by building new plants faster than ever before. This will strengthen UK energy security by reducing dependence on imported fossil fuels, provide more affordable electricity, and grow the economy."

The Philippines does not have to reinvent the wheel in its commitment to reduce greenhouse gas emissions, particularly with exemplary policies and real-world successes (as demonstrated by the UK) that could be applied in the country in the manner that is suitable to our circumstances and constraints.

Framework for Discussion

Objectively speaking, the Strategy presented in the preceding section seems audacious. For the harshest skeptics, I posit that there are two (2) particularly challenging issues in connection with the Strategy:

- Interim storage and permanent disposal of radioactive waste of SMRs and

- High cost of electricity of SMRs.

Further, I would maintain that if these two (2) challenges are addressed, then the Strategy is actually no less audacious than any number of strategic economic initiatives that have resulted in the economic "miracles" we recognize today as Taiwan, South Korea, Singapore, among others.

Challenge 1 Interim Storage and Permanent Disposal of Radioacdtive Waste

Arguably, the most challenging issue of all is the disposition of nuclear waste, which is an undesirable but unavoidable by-product of SMRs. Today, after more than half a century of commercial operations of nuclear power plants all over the world, not a single country on the planet has a fully commissioned Geological Disposal Facility or GDF for the permanent disposal of radioactive waste produced by nuclear power plants--NOT ONE.

Fortunately, Finland has taken the lead in takling this challenge. The Onkalo Geological Disposal Facility (GDF) began testing and trials in August 2024, placing empty fuel canisters inside the burial chambers. It is currently in the process of receiving final approval to begin operating. The first GDF is nearly done and it can and will be done by other countries. No doubt, the need to reduce and eventually eliminate fossil fuel power plants to reduce the emissions of greenhouse gases and mitigate the existential threat of climate change is now turbocharging the development of renewable power plants, energy storage facilities AND new generation SMRs worldwide, which, in turn, is compelling countries with nuclear power to finally address the permanent disposal of radioactive waste with GDFs. Today, Canada, United Kingdon, France and Sweden have advanced plans to build a GDF, although none of these countries have decided on any definitive site to date. Nobody said it was going to be easy but the point is, it can be done and more GDFs will follow after Onkalo.

The next question is, who will pay for the GDF in the Philippines? It stands to reason that the entities that will use the GDF should pay for it. To start, the SMRs in the Philippines should finance, build, own and operate the GDF in the Philippines as an integral and inseparable part of their entry into the nuclear energy program of the country. However, the SMRs need to be paid for building and operating the GDF. This can be done with a payment scheme similar to the one used by the US Federal Government to fund the Yucca Mountain nuclear waste repository* (a GDF). 27% of the cost was paid by taxpayers for the disposal of naval and weapons nuclear waste and 73% of the cost was paid by consumers of nuclear-powered electricity. There is no nuclear defense waste in the Philippines; therefore, 100% of the cost of the GDF would be paid by consumers of nuclear powered electricity; namely, the HDCs and (maybe) the Philippine consumer. More details below.

*The Yucca Mountain project was eventually canceled due to state and federal politics, and a lack of political will--an utter waste of US taxes and an example of what should NOT be emulated in the Philippines.

Because the Philippines stands to gain from getting a slice of the global HDC industry into the country (by permitting SMRs to supply power to HDCs), the Philippine government should provide the site for the GDF free of charge. This contribution, which the Philippine government can afford, also conveys the message that the Philippines is serious about the disposal of radioactive waste in the context of its nuclear energy program.

If the HDCs in the Philippines do not foot the bill for the GDF (or at least their part of the bill for the GDF) or if the Philippine government will not provide the site for the GDF free of charge, then there is no Strategy to begin with. End of story.

Challenge 2 High Cost of Electricity of SMRs

This second challenge is, not surprisingly, actually related to the cost of the GDF to be shoulderd initially by the SMRs and, in turn, to be shouldered by the end-users purchasing power from the SMRs--in this case, the HDCs and, maybe (but not necessarily), the Philippine power consumer.

The two (2) diagrams below illustrate the following scenarios:

- A nuclear energy program in which SMRs do NOT provide any load balancing to the grid and, therefore, supply exclusively the electricity requirements of the HDCs. In this first scenario, the electicity supplied by SMRs and purchased by HDCs is a commercial transaction entered into by two business entities voluntarily. If HDCs, in their need to expand their enterprises globally, voluntarily pay a higher price for electricity supplied by SMRs, that's their business. The only "imposition" on the Philippine power generation sector is to beef-up its reserves to provide adequate back-up power to the HDC complexes--which is really not an imposition because this scenario only forces the grid to plan for reserves according to best global utility practices that benefits all power consumers in the country. To be clear, in this first scenario, the Philippine power consumer will continue to pay the price of electricity according to the status quo as if the SMRs did not exist in the country, simply because all of the electricity produced by SMRs are sold exclusively to HDCs at whatever price these parties have agreed upon.

- A nuclear energy program in which SMRs provide load balancing to the grid and, therefore, would entail supplying electricity to the grid, which is likely to increase the price of electricity of Philippine power consumers. That said, the more renewable energy plants are built in the Philippines, the more energy storage facilities will also be required to balance the load of the grid. To date, the cost of energy storage is relatively expensive, whether it's a battery energy storage system, a gravity energy storage system (like pumped-storage hydro and Energy Vault), a molten-salt energy storage system (which can be configured with an SMR), among other energy storage systems. Hence, as energy storage systems are built into the grid to balance the intermittent and variable output of an increasing number of renewable energy plants, the price of electricity of Philippine power consumers will increase anyway. In light of this unavoidable economic reality, the more appropriate question is, does an SMR based energy storage system (like the molten salt energy storage system of Terra Power's Natrium plant) produce electricity for load balancing at a more competitive price compared to non-nuclear energy storage systems? Terra Power claims that the Natrium's molten salt energy storage system is more resilient, flexible and cost-effective than current grid-scale battery storage technology. This claim will be verified after Natrium is commissioned in 2030.

Scenario 1--WITHOUT SMR Load Balancing

Scenario 2--WITH SMR Load Balancing

Provided the cost-effectiveness of a nuclear based energy storage system (NES) is at par or more competitive than a grid-scale battery energy storage system (BES), it behooves energy planners in the Philippines to integrate various energy storage systems (NES, BES, among others) as part of a robust and resilient grid with an increasing mix of renewable energy plants.

Using the Natrium plant as an example, which is a 345 MW baseload plant with the capacity to provide an additional 155 MW (an additional 45% of baseload capacity) over a period of 5.5 hours (i.e., 852.5 MWh of energy storage), then we can extrapolate that the 4,800 MW of baseload SMRs contemplated in the first component of the Strategy, configured with the molten salt energy storage system (the second component of the Strategy) could provide an additional 2,160 MW over a period of 5.5 hours (i.e., 11,880 MWh of energy storage).

To put this figure (11,880 MWh) in perspective, let's use SPNEC's 3,500 MW solar farm and its 4,000 MWh battery energy storage system as an example. Assume the solar farm generates close to 3,500 MW for 4 hours during the peak of a sunny day (without clouds) and a fraction thereof (say 1,500 MW) for the balance of 6 hours. This would be equivalent to 23,000 MWh of electricity generated, which is consumed by customers during the day. At night, the solar farm will be off. Further, assume the power consumption of the same customers over the next 12 hours (dusk, nighttime and dawn) is only 70% of 23,000 MWh (or 16,100 MWh). The combined energy storage of SPNEC (4,000 MWh) and the SMRs (11,880 MWh) or a total of 15,880 MWh would be just enough to fulfill the demand.

This is a highly simplified scenario of how the load of the grid would be balanced, as the current power generation mix is still mostly comprised of fossil fuel plants. However, as more renewable plants and less fossil fuel plants comprise the generation mix, more energy storage facilities will be required and the above example of dispatching energy storage systems at night (during cloudy days and days without wind) will become the norm. The point is, the integration of energy storage systems with all of the SMRs contemplated in the Strategy (only 4,800 MW of baseload capacity with 11,880 MWh of energy storage) is not nearly enough for the national grid. It will only be a portion of a much larger amalgamaton of various types of energy storage systems that will eventually be required to balance the load of the grid. All of which will likely increase the price of electricity.

Should the Philippine government decide to take the path of least resistance, then only the first component of the Strategy would be pursued and "Scenario 1--WITHOUT SMR Load Balancing" above would apply. It involves only US companies with respect to both SMRs and HDCs, albeit establishing enterprises on Philippine soil. It's uncomplicated, even if US Federal Government subsidy is required to implement the Strategy in the Philippines.

On the other hand, if the nuclear-based energy storage system of Natrium proves to be cost-effective compared to other grid-scale energy storage systems in the market and the Philippine government decides to take a more strategic approach, then both the first and second component of the Strategy would be pursued and "Scenario 2--WITH SMR Load Balancing" above would apply. That said, because a portion of the electricity generated by the SMRs will be consumed by Philippine consumers, seeking US Federal Government subsidy, if required to implement the Strategy in the Philippines, may be more complicated (but not insurmountable).

US Federal Government Subsidy

There is one all encompassing element that has enabled the new generation of SMRs to be commercialized in the United States--subsidies from the US Federal Government. Perhaps the more appropriate description is "on the cusp of commercialization" because probably not all of these SMR companies will cross the proverbial finish line.

In its Q2 2024 Company Update, Oklo reported the estimated range of the Levelized Cost of Electricity (LCOE) of its SMR from US$40 to US$90 per MWh. These figures are qualified with the following fine print quoted in its entirety as follows:

"Estimates for Oklo LCOE range assume: (i) All regulatory approvals have been obtained on expected timelines; (ii) a run-rate of 20 units to achieve NOAK unit economics; (iii) 30% ITC with 90% transferability; (iv) power outputs of 15-50 MWe; total refueling capital expenditures over the expected 40-year life of the Aurora powerhouse assumed to be $53-84mm; (v) excludes overnight cost contingency or decommissioning cost; (vi) levelized average lifetime cost approach, using the discounted cash flow (“DCF”) method; and (vii) a weighted-average-cost of capital of 8% based on the International Energy Agency sensitivity analysis range of 4-8%."

Although the above fine print suggests that Oklo's SMRs, once deployed in the market, are bonafide commercial undertakings (albeit with tax incentives, which is not unusual), there is the glaring exclusion of "overnight cost contingency or decommissioning cost"--both of which could be show stoppers.

Rather than speculate on the actual meaning of these exclusions, let's just assume that:

- Oklo, like other SMR companies, will have cost overruns on their SMRs. What really matters is that these cost overruns do not surpass that point at which SMRs and HDCs cannot agree on the electricity price in their power purchase agreements. This will be the end of the alliance of SMRs and HDCs and the end of the Strategy. For example, due to substantial cost overruns, the first expected commercial SMR in the United States was scrapped by NuScale in Novmeber 2023. Although a major setback to the advanced nuclear industry, NuScale and its peers in the industry continue to push forward toward the commercialization of SMRs and right behind them is a global economic juggernaut--the HDC sector.

- Oklo has not factored into its SMR's estimated LCOE the cost of the GDF, which would not be unusual in the context of the United States. Oklo would only be one of several SMR companies plus the entire group of legacy nuclear power plants in the US. In the context of the Strategy in the Philippines, the SMR company or companies (in a consortium) in the Philippines would be responsible for building and operating the GDF in the country, which is not the case in the United States. How would this be done in the Philippines? More particularly, how would the GDF be funded?

SMRs need to be fundamentally commercial enterprises and competitive in the context of an electricity market that values their contribution to climate change mitigation. To level the playing field, certain institutional prerequisites need to be in place, including, but not limited to, fiscal/tax incentives, carbon price support mechanisms and selective VAT exemption on the sale of electricity from green sources. This may also entail policy requiring consumers to pay a slight premium for electricity generated from SMRs to provide the necessary funds to built and operate a GDF. Finally, an up-front funding "subsidy" to get the GDF started.

In Scenario 1--WITHOUT SMR Load Balancing, the only parties involved in the production and purchase of electricity are SMRs and HDCs, respectively, which are US entities. Whatever electricity price agreed upon by the parties in their power purchase agreements is their business and does not affect the price of electricity of Philippine consumers. What is critical to the Philippines is that embedded in said electricity price is a component specifically alloted to build and operate the GDF. Moreover, because the parties involved are US entities, if US Fededal Government subsidy is required to achieve the "right" electricity price, then such US subsidy should be seamlessly embedded in the deal structure of these US companies without any need for the participation or involvement of the Philippine government other than the normal course of facilitating strategic investments into the country.

In this case, US Federal Government subsidy (if any) would be justified, given that US taxpayers (including the SMRs and HDCs themselves, which are US entities paying taxes to the US government) would be supporting US enterprises (SMRs and HDCs) which happen to have facilities on Philippine soil (and also paying taxes to the Philippine government).

Because it is in the best interest of all stakeholders (SMRs, HDCs, the Philippines in general) to have an operational GDF in the country sooner than later, the contemplated "subsidy" may in fact be an advance of funding from the US Federal Government to build the GDF that would ultimately be paid back by the SMRs to the US government (by way of the portion of the tariff in the PPAs specifically allotted to build and operate the GDF), albeit by installment over the 40 to 60 year operational life of the SMRs.

In Scenario 2--WITH SMR Load Balancing, a portion of the SMRs electricity production (say 11,880 MWh per day from energy storage component of the SMRs based on the Natrium's configuration) is exported to the grid for load balancing and consumed by Philippine customers. Hence, in Scenario 2, there are two (2) groups that are purchasing and/or benefiting from the electricity production of the SMRs: the US entities (SMRs and HDCs) and the Philippine consumer.

The contemplated payment mechanism in Scenario 1 to fund the construction and operation of the GDF would apply, except that the electricity exported by the SMRs to the grid (and consumed by Philippine customers) will also have a portion of the tariff specifically allotted to fund the GDF--no different from portion of the tariff in the PPAs between the SMRs and HDCs for the same purpose. As such, a slightly larger GDF that has the capacity to permanently store the radioactive waste of 4,800 MW of baseload capacity AND 2,160 MW of load balancing capacity* (based on Natrium's configuration) will essentially be paid by the HDCs and the Philippine consumer, respectively--with the SMRs as collector and remitter of payment to the US government.

*2,160 MW over a period of 5.5 hours translates to an equivalent baseload capacity of only 495 MW; hence, the share of the Philippine consumer to fund the slightly larger GDF will be roughly 10%.

The question is, would the US Federal Government (i.e., US taxpayers) be willing to advance the funds to built a GDF in the Philippines sooner than later when the primary beneficiary of 10% of the design capacity of the slightly larger GDF is the Philippine consumer--NOT US entities.

Consider the Onkalo GDF in Finland having a total project cost of US$1.07 billion and the capacity to store 5,500 metric tons of vitrified high-level waste--enough to store all the waste from Finland's five nuclear power plants (with a total capacity of 4,400 MW) over their entire life cycles.

The equivalent baseload capacity of the SMRs with energy storage for load balancing is 5,295 MW (4,800 MW + 495 MW), which would require a GDF with 20% more capacity* than the Onkalo GDF and a corresponding cost of roughly US$1.3 billion. Assuming a 50% contingency, due to uncertainties in the parameters of radioactive waste produced by SMRs*, this figure amounts to a US$2 billion price tag for a GDF in the Philippines, of which 10% or US$200 million would be paid for by the Philippine consumer over a period 40 to 60 years; that is, if the US Federal Government agrees to fund the entire US$2 billion price tag up front. Theoretically, if every man, woman and child in the Philippines (population of roughly 120 million) were to pitch-in US$1.67 today, the Philippine consumer's share of the GDF would be paid on day 1.

*There are conflicting opinions on the radioactive waste generated by SMRs. Taek Kyum Kim, a senior nuclear engineer at the U.S Department of Energy’s Argonne lab in Lemont, Illinois, states "When it comes to nuclear waste, SMRs are roughly comparable with conventional pressurized water reactors;" whereas, Lindsay Krall, the lead author of a study published in the Proceedings of the National Academy of Sciences, states "A comparison of SMRs shows that designs cooled by water, molten salt and sodium will increase the volume of nuclear waste requiring management and disposal by factors of two to 30."

Consider the recent grants of the US government to the Philippines in connection with the military cooperation between the two allied countries. These include US$500 million to help in the ongoing modernization program of the Armed Forces of the Philippines (AFP) and the Philippine Coast Guard (PCG) and US$128 million to fund important EDCA infrastructure projects. Based on these recent US government grants to the Philippines, seeking advanced funding from the US Federal Government of US$200 (or more if necessary) for the Philippine consumer's share of the GDF appears reasonable. It's not even a grant (which is a giveaway with strings attached) but advanced funding that will be paid back over time.

Industrialized nations have been the primary contributors to greenhouse gas emissions since the Industrial Revolution, leading to global climate change. These nations have enjoyed the economic benefits of fossil fuel-driven development, and their emissions are responsible for much of the environmental degradation that is now affecting vulnerable countries.

The idea that those who have contributed most to the problem have a greater moral obligation to help fund solutions. Since developing countries have contributed far less to the current levels of global emissions, they should not bear the same burden of the transition to a low-carbon economy. Because industrialized countries generally have greater financial resources and technological expertise to facilitate the transition to renewable energy and developing countries often lack the financial means, infrastructure, and technical capacity to shift away from fossil fuels without external support, it is incumbent upon wealthier nations to assist poorer nations in their efforts to combat climate change and transition to clean energy sources, and it is ethically justifiable for them to do so as part of a global solidarity effort. Hence, advanced funding from the US Federal Goverment for the GDF in the Philippines would constitute a concrete model of such assistance, which is actually quite nominal in the whole scheme of things and could be emulated globally.

Why HDCs (Hyperscale Data Centers) in the Philippines?

It's not rocket science. The global HDC industry is big (projected to hit US$1 trillion in 2033), essential (in every aspect of industry, commerce and the everyday life of most of the entire population on earth) and growing fast (projected CAGR of nearly 28% from 2023 to 2032). North America (US and Canada) currently holds the largest market share but Asia Pacific is expected to grow at the fastest rate (from 2023 to 2032) due to growing industrialization and developing markets.

By 2026, China and Hong Kong alone are projected to generate 50% of data center revenues in Asia Pacific (APAC), followed by Singapore, Australia and Japan with 37%. Even among countries in Southeast Asia, the Philippines is projected at only 2%. We can do much better.

The Philippines is sandwiched between North America (the largest market share in the world) and China (the largest market share in APAC), and in the middle of the highest growth region (APAC) over the next decade. Like our value in the military strategem of the US in APAC, we can position the country's HDC sector as a virtual extension of the US in APAC--as if Google, Meta, Microsoft and Amazon were setting-up their nuclear powered HDCs in North America but in the Philippines instead.

And, by the way, there is already an undeclared war between the US and China in the realm of submarine cables. Case in point, I quote the following excerpt from Manolo Quezon's article dated May 11, 2023 entitled "Submarine cables: An undeclared war."

"The Pacific Light Cable Network (PLCN) began as a Chinese majority-owned submarine cable system initially designed to connect Hong Kong, Taiwan, the Philippines and the US. PLDC (Pacific Light Data Communication) also had two major American partners: Google and Meta (formerly Facebook). In 2020, Team Telecom of the US Department of Justice recommended disapproval of its undersea cable connection to the US. So Google and Facebook refiled their application to connect Taiwan and the Philippines to the US, abandoning the Hong Kong portion, and “without ownership and control by a Chinese entity.” By January 2022 this was approved and in February, the Dr Peng Telecom Media Group, a Chinese stakeholder in PLDC, sold its stake at a loss, replaced by a Canadian investor."

Manolo aptly observes, "You can connect to China or America but not both, as undersea cable battlelines are drawn." Not eactly but the alliance of the Philippines and the US should be fully exploited in terms of managing data to and from China to buffer US HDCs in the country from the Evil Empire. This has to count for something in contrast to some of our Southeast Asian neighbors that are treacherously flirting with China and Russia in BRICS. To put it bluntly, Malaysia and Indonesia are cozying up to China and Russia yet US HDCs are coming in droves to Johor Bahru and Batam. Of course it's because of Singapore's proximity but there has to be another way--and that could be the Philippines. We just need more submarine cables like PLCN to turbocharge and secure (particularly with respect to China) our broadband capacity to the rest of the world.

This is consistent with the following statement of the Center for Strategic and International Studies (CSIS, a bipartisan, nonprofit policy research organization of the US government that, among other things, defines the future of US national security) advocating the global role of the US in advancing digital technology as follows:

"Digital transformation has defined the modern age. Digital connectivity serves as an opportunity to expand geopolitical influence as appetite and need for telecommunications infrastructure and broadband deployments in developing markets grow. Bridging the digital divide is imperative for countries to unlock economic growth and more aptly compete in an increasingly online world. The impact of great power competition between the West and the PRC (China) to bridge the digital divide in developing countries is complex. How (and how responsibly) developing countries choose to meet their modernization goals could have far-reaching implications for the sustainability and effectiveness of development gains as well as for geopolitics." This is the Philippines' cue to work with the US in bridging the digital divide in Asia Pacific. Arguably, there is no better way to execute in a substantial and relevant scale than through this Strategy.

Supposing the Philippines targets and secures only 5% of the US$1 trillion global HDC market by 2033, that would constitute a US$50 billion per annum industry in the country--just enough to offset the losses associated with the imminent decline of the country's BPO industry.

In the sample configuration of a 400 MW nuclear powered HDC complex on an 80 hectare site in Nampicuan, Nueva Ecija, Philippines (the Site), the total project cost would be in the magnitude of US$6 billion. This is based on current total project cost estimates for a 100 MW HDC at nearly US$1 billion; whereas, preliminary estimates on SMRs today are in the range of US$5 million per MW--much higher up-front capex and lower opex compared to fossil fuel plants that is typical of nuclear power plants. The sample configuration multiplied 12 times (4,800 MW in the Strategy) translates to US$72 billion of foreign direct investment (FDI) in the Philippines--a substantial contributor to the country's FDI with a modest annual inflow average of only US$8.6 billion (10-year average from 2014 to 2023, see graph below).

Fast forward to 2040 and beyond, as 15,000 MW of coal plants are decommissioned and repurposed to 15,000 MW of nucleared power HDC complexes (on the exact same decommisioned sites), another wave of FDI would ensue to the tune of US$225 billion (value in 2024). All in all, the first and second wave of nucleared power HDC complexes in the Philippines (this sector alone) could potentially infuse US$300 billion (value in 2024) of FDI into the country over the course of three decades. In the process, the Philippines would also be securing its energy independence and doing its part to mitigate climate change.

Supporting data below:

The global hyperscale data center market size was estimated at USD 80.16 billion in 2022 and is expected to hit around USD 935.3 billion by 2032, poised to grow at a compound annual growth rate (CAGR) of 27.9% during the forecast period 2023 to 2032. (Source: Precedence Research)

Hyperscale Data Center Market Share, By Region, 2022 (%)

2026 Forecast of Percentage of Revenues of Data Center in Asia Pacific by Country

Source: Global Information Inc.

How competitive are SMRs in the Philippines?

How competitive is the price of electricity of Oklo's SMR in the Philippines? (I am using Oklo as an example due to the availability of data disclosed by Oklo in the public domain and because Oklo is representative of other SMR companies in the United States.)

In the context of the Strategy, the price of electricity of SMRs should be evaluated in relation to the power purchaser, which, in this case, are (1) the HDCs in the Philippines and (2) the Philippine power consumer.

The Case of HDCs